THEY changed.

And I really don't understand WHY

THEY changed.

I believe

THEY changed because

THEY are scared. That is the only reason I can think of, really.

Scared that things would get out of hand to the upside, with asset prices higher than their cash flows justified, and then one-two-jab-uppercut to the downside. Swiftly. When things get parabolic you know that late-comers show up just to be the last buyers. It's beautiful. People in the market get trapped. But hesitate to realize a quick, small loss.

So, ladies. Basically we lived, in the past 3-4-5 years, on monetary morphine, either through ZIRP, or on asset-buying programs, or on buy-the-dip "whatever it takes" dovish speeches by policy makers. Attempts at creating credit. Attempts at suppressing volatility. Attempts at keeping negative real interest rates that pushed capital into whatever gets them cents per month.

But that now changed.

THEY changed.

I never believed the world would accelerate upwards and THE GREAT DEBT PROBLEM could be solved.

I am of the opinion that there is no good solution for the problems the world is currently facing.

This problem is simply

TOO MUCH DEBT. Debt which was used to build excessive industrial capacity or used to buy things such as bytes that end up in the pocket of shareholders of Google (sells ad-clicks), Apple (sells design and bytes through music and movies), among others, etc. To consume things that didn't generate cash flow which could be used to pay debt down. Ouch.

The world changed too. There aren't enough jobs for people anymore. Just for machines, automation and capital. Not as many jobs as we have unemployed. THAT, my friend, won't change. We have reached the labor-deflation era. There will be spare capacity in labor. Until, perhaps famine, or disease, or war reduces population? Tough.

The only reason I can think of right now for

THEM to have changed is that they gave up on trying to generate inflation through the asset-price transmission mechanism, where higher asset prices ignited animal spirits that made citizens of the world consume useless things that aren't used to produce cash flow enough to pay down debt.

So

THEY thought "well, maybe we'll stop for a little bit, see what the reaction of financial assets is". And it has been a horror show.

And that's what

THEY did. One-by-one.

Fed is tapering. And I really don't think it is because he believes the US will speed up from here in terms of nominal growth.

The

ECB recently got a bit more hawkish too after bring us a rate cut. But not negative interest rates.

The

BOJ also paused. Basically Abe got what he demanded from his Central Bank and will try, through political reform and fiscal stimulus, his other arrows. Monetary policy on hold until further signals from the japanese economy.

and...

PBoC! The chinese are trying to engineer a soft-landing, trying to rebalance their economy. Away from credit intensive infrastructure and manufacturing capacity, towards services and consumption.They're squeezing excess credit from the system, trying to make credit available for those who have productive investments.

THEY, at least now, don't seem to be on the investors' side. Not yet. Not at these levels in asset prices in Japan, US, Europe. So be very careful. Until

THEY come back with their white doves... be careful.

THEY, the Central Banks and governments, have tried to generate inflation / nominal growth through fiscal and monetary programs for some time after the crisis.

It worked for some time. Now if you look at global aggregate nominal growth it is basically the same story.

So in the past few years some global agents have been trashing their currencies to try to steal some growth, generating some internal inflation so that nominally it would be easier to pay off debt.

The problem is that when that happened it was at the expense of someone's lower inflation and nominal growth.

I'm not going into #s here because I am lazy. But the US devalued their dollar, pushing their real interest rates lower and lower and forcing global agents to reach for yield elsewhere.

That made capital flow from the US into many countries, scooping up assets while pushing their currencies higher. At first these other countries got a boost in growth, in asset prices, etc.. Then what happened?

Basically either some inflation showed up and they were forced to tighten monetary policy or try to fight these flows with some form of capital control, etc. Then, for others, with much more expensive currencies they were forced to export deflation through lower prices of goods, in order to compete with peers in global trade.

Gold, which I am actually fond of, has lost its lure. Why? I think it is the canary in the coal mine. It is telling me that

THEY lost the battle to inflation and debt-deflation will be the way to actually solve the TOO-MUCH-DEBT problem. If Gold is supposed to maintain its holders purchasing power... maybe prices are heading into a steep fall from here, when Gold stabilizes, outperforming. Who knows.

I think what

THEY are doing, being hawkish at the margin, is very dangerous.

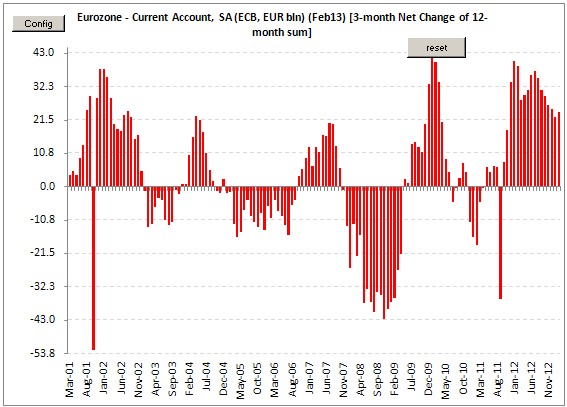

First there was the correction in, as example, the Current Accounts of the US and of the Eurozone.

And now all the hawkish talk. First a simple flow issue.

And now a monetary policy stance issue.

All that capital that flowed into the Brazils, the Chinas, the South Koreas, etc... is now saying good bye and heading back home.

The consequence is rather easy to spot:

I didn't have time to do the same for these countries' interest rates curves, but, mate, we have seen some gigantic, 2008-style, moves in many countries yield curves of late, response to the massive reduction in sharpe-ratios, of the carry trades.

Basically

THEY, being hawkish at the margin, released the yield-volatility genie out of the bottle, pulled capital from whatever country benefited from easy-money policy from 2009-2013 back to their country... and FX moved, increasing the volatility of returns of the carry trades. The sharpe (return / volatility) decreased.

Are you going to sit 2-3 years holding a foreign currency bond in order to recoup FX losses through carry? Do you know if the FX rate will move further against ya? Well... no one does. So shoot first, run afterward... and I wouldn't even ask the questions! At least not for a long time.

So to finish it off as I need to sleep eventually...

Markets stared at the price action of the S&P 500 and some European equities, now the Nikkei, and forgot to observe what was going on in other parts of the world. They were slowly, then suddenly sliding down. And there are no signs of inflation to help pay down the TOO-MUCH-DEBT problem.

Now these massive moves in their FX and long-end rates will speed up the process of credit crunch and confidence loss. That's lack of demand of sorts.

In the US people were starting at their equities and corporate bonds and forgot to pay attention to their Fiscal Drag.

I strongly believe we have seen the lows in US Credit Yields and US Credit Spreads because this change in stance on part of the Fed, despite me not believing growth will come, puts the Fed in check. That means, if 1/ growth really comes, yields will remain higher because Fed will have to taper or 2/ if growth disappoints, considering the poor momentum in US growth, it means recession and default probabilities going up.

So either way.. Credit stays in check. And credit discounts future cash flows.And funding costs. So it leads equities.

I now believe, as I mentioned earlier here, on tweets, that as soon as asset prices stay in check, giving back a good chunk of their gains, confidence levels will retreat and, with higher discount rates, the economy will show a severe slow down and Bernanke will be proven without clothes under water. And in cold water... what a shame!

Many people have been waving the "real yields higher mean the economy is finally getting back on its feet" flag. Man... Call me crazy, but I think that is completely wrong. Nominal yields have been going up and inflation expectations have been trending down for some time now... so.. this smells really bad in my opinion.

"Market are good at predicting recessions because they cause recessions" (Soros).

This is no financial advice, but cash, in this environment, is king if you can't go short! It shines.

Time to sleep. It's almost 1am.

I'll review this post later in order to add/correct any confusion. Now I am tired and very worried.

Oh, before the Publish button, this chart with NYSE Net-Debt x the SPX and a few others that have kept me from turning light off to sleep.

In red... pretty tepid #s.